Bonds In Conversation : Run Lola, Run – Newton’s Law

Watching the market actions unfold into the half year closing, I remember a movie I watched over a decade ago. The beauty of Run Lola, Run, besides the chick (i like her because she looks real) from Bourne series, is that there were 3 different endings laid out depending on the sequence of events and choices Lola made while she was running.

It is pretty apt for this week as we concludeTaper Part 2 this month end. Part 1 – Acknowledging the Taper is over. Basic reactions were registered, the end of the EM carry trade, the rise in US Treasury yields, the commodity bubble bursts and a small correction in the S&P 500.

Part 2 – Central banks reactions were largely nonplussed, sending the markets into another spiral down only to buck up for the month end and semi annual window dressing ramp up.

Now what ?

Part 3 awaits – Investor behaviour in the immediate future.

The Fed is still monetising like crazy, in case you are not aware. Just another 3.5 or so billion last night. That is liquidity albeit temporary liquidity, as we now know it.

Newton’s First Law of Motion :

An object that stays at rest, remains at rest and an object that is in motion, remains in motion. Unless a external force acts on it.

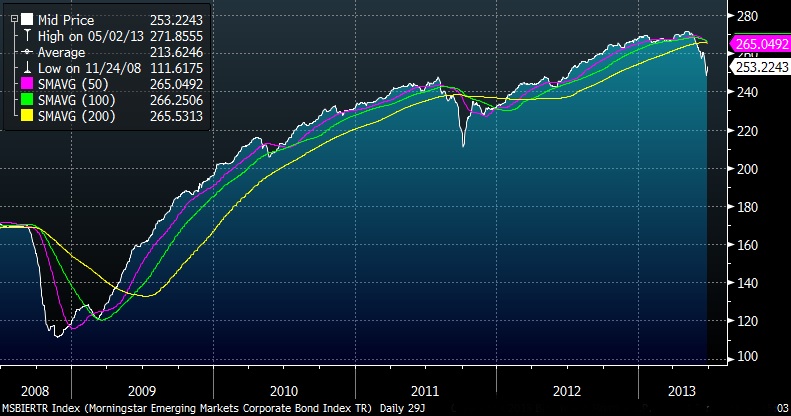

An FT survey indicates that 32% of fund managers plan to sell Asean equities in the next 2 months. We can assume the same for bonds. Credit spreads have widened out approx. 10-15% according to the Morningstar EM index.

Singapore corporate bonds are still holding on to their credit gains with their prices adjusting for just higher interest rates. In a relative value world, institutional investors can start buying USD bonds and swapping into SGD when local prices and spreads do not make sense (the only prevention is USD/SGD going higher). Or worse, they could just start selling SGD bonds when redemptions strike.

Banks just do no have enough lines to stomach all the excess papers, notably those big issues like Genting and bank perps (some of which do not have interest rate re-fixings like OCBC 4%).

I notice Olam quite bashed for the week, along with Swibers and Cenchi too. Long end >2022 maturity papers like Spower 2032 etc, also did not fair too well.

EM company bonds – Trikomsel took a heavy beating, falling almost 1% which is expected given that it was way too tight when it was issued. The Tatas’ are holding out real well though.

I leave with a quote from a WSJ article, This Rally Doesn’t Mean The Selling is Over.

“investors have been conditioned to believe that every short-term market pullback is merely a buying opportunity for the next leg up in an endless bull run. One day, they’ll be in for a nasty surprise.”

Indicative prices (all unverified and note for potential errors in the yields – I did a few sanity checks here and there)

Note : The Gain/(Loss) column refers to the gains in % points the bond has made over the credit spread it was issued at. It does not refer to the gains for the week. Also, they should not be used to evaluate whether the bond is over or under valued but rather, serve as a point of reference.