Ad Hoc Commentary – rate hikes irrelevant as monetary transmission is broken

Yours truly apologize for not writing in recent times. Today is Fed Powell’s first meeting. Markets are very different today compared to the last Fed rate hike cycle of 2004-2006. Today,

- Fed Funds is irrelevant because banks have sufficient reserves.

- Libor is irrelevant because very few trade unsecured post-Lehman.

- Libor versus Fed Funds spread as a measure of monetary policy transmission is largely irrelevant because the markets are inactive, some say nearly dead.

What matters today from an interest rate perspective is:

- Interest on Excess Reserves (IOER) for entities that can hold reserves

- Fed Reverse Repo Rate (RRP) for entities that cannot hold reserves

- FX Swap implied rate (FXS) for everyone else

- FXS versus RRP spread as a measure of monetary policy transmission. In fact, there is a foreign RRP facility but that is only for the club.

If you look at FXS rates, Dec 2017 was one of the worst in recent memories. As the chart below shows, the difference between EURUSD 1m implied rate and EURIBOR 1m is 250 bps at the end of last quarter.

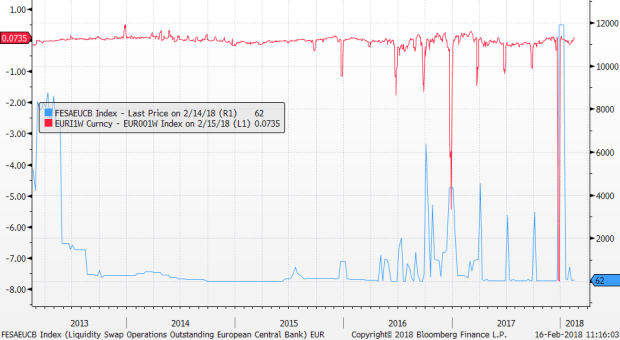

Looking at the 1w tenor, you can see that the EUR 1w implied rate spiked to nearly 800 bps last year-end (red line). At the same time, the ECB tapped the central bank FX swap lines to relieve the US dollar shortage in Europe (blue line) in the tune of 12 billion dollars.

The Fed is paying attention and it is surprising that Fed watchers are not talking about this as much as they should. Quarterly spikes in FXS is effectively a broken monetary transmission. It is rate hikes of 700 bps without the Fed getting involved. To fix this, the Fed needs to rollback two key piece of regulations:

- Enhanced Supplementary Leverage Ratio (eSLR)

- Volcker Rule

First, eSLR must be rolled back because it dilutes the return on equity for banks that engage in low margin business of monetary transmission, i.e. borrowing US dollars onshore and lending it offshore in the FX swap market. Chairman Powell noted on Feb 28:

“The leverage ratio can deter banks…from engaging in low-risk wholesale activities, particularly the custody banks,” he said. “Our preference for the way to do that is to just recalibrate the enhanced supplementary leverage ratio.” https://www.wsj.com/articles/powell-backs-senate-plan-to-raise-threshold-for-systemically-important-banks-1519758028

Custody banks are probably mentioned because custodians hold a disproportionate amount of reserves at the central bank earning IOER. These reserves could be better used in fixing the monetary transmission – a low-risk wholesale activity. Instead of parking it at the Fed at IOER, custodians should lend to the wider economy at FXS implied.

Two slow moving titanics are making this urgent:

- Trump corporate tax plan draining US dollars liquidity offshore back to onshore.

- Fed shrinking of balance sheet, which will accelerate to 50 billion dollars per month at the end of this year. In other words, the central bank will drain 50 billion of reserves from the banking system every month.

Since liquidity is being drained by corporates and the Fed, custodians needs to come in to fill the vacuum. Else we will likely have a monetary crisis, and interest rates will rise much faster than the three or four rate hikes in the Fed dot plot.

Second, the Volcker rule must be repealed. The shortage of US dollars is a shortage of balance sheet to intermediate between the suppliers of US dollars (mainly onshore) and the consumers of US dollars (mainly foreign investors who wants to buy US assets usually on a hedged basis). Volcker rule causes problems because it bans speculative books. In other words, banks must run matched books, i.e. borrow via FXS and lend via FXS. This makes monetary transmission expensive because an unregulated third-party intermediary must get involved to do the speculative book leg – i.e. borrow from cash pools and lend on via FXS. The Fed Vice Chairman is paying attention: “Federal Reserve Vice Chairman Randal Quarles says U.S. financial regulators are working quickly to make “material changes” to the Volcker Rule” https://www.bloomberg.com/news/articles/2018-03-05/volcker-rule-to-undergo-material-changes-fed-s-quarles-says

Given the broken monetary transmission today, it really does not really matter if the Fed hikes 25 or 50bps. It also does not really matter if the Fed’s infamous “dot plot” shows 3 or 4 rate hikes in 2018. What really matters is to fix the broken monetary transmission in a year when offshore US dollar liquidity is being drained by both US corporates and the Fed herself.

Good luck in the markets.

Ad Hoc Commentary – rate hikes irrelevant as monetary transmission is broken

Yours truly apologize for not writing in recent times. Today is Fed Powell’s first meeting. Markets are very different today compared to the last Fed rate hike cycle of 2004-2006. Today,

What matters today from an interest rate perspective is:

If you look at FXS rates, Dec 2017 was one of the worst in recent memories. As the chart below shows, the difference between EURUSD 1m implied rate and EURIBOR 1m is 250 bps at the end of last quarter.

Looking at the 1w tenor, you can see that the EUR 1w implied rate spiked to nearly 800 bps last year-end (red line). At the same time, the ECB tapped the central bank FX swap lines to relieve the US dollar shortage in Europe (blue line) in the tune of 12 billion dollars.

The Fed is paying attention and it is surprising that Fed watchers are not talking about this as much as they should. Quarterly spikes in FXS is effectively a broken monetary transmission. It is rate hikes of 700 bps without the Fed getting involved. To fix this, the Fed needs to rollback two key piece of regulations:

First, eSLR must be rolled back because it dilutes the return on equity for banks that engage in low margin business of monetary transmission, i.e. borrowing US dollars onshore and lending it offshore in the FX swap market. Chairman Powell noted on Feb 28:

“The leverage ratio can deter banks…from engaging in low-risk wholesale activities, particularly the custody banks,” he said. “Our preference for the way to do that is to just recalibrate the enhanced supplementary leverage ratio.” https://www.wsj.com/articles/powell-backs-senate-plan-to-raise-threshold-for-systemically-important-banks-1519758028

Custody banks are probably mentioned because custodians hold a disproportionate amount of reserves at the central bank earning IOER. These reserves could be better used in fixing the monetary transmission – a low-risk wholesale activity. Instead of parking it at the Fed at IOER, custodians should lend to the wider economy at FXS implied.

Two slow moving titanics are making this urgent:

Since liquidity is being drained by corporates and the Fed, custodians needs to come in to fill the vacuum. Else we will likely have a monetary crisis, and interest rates will rise much faster than the three or four rate hikes in the Fed dot plot.

Second, the Volcker rule must be repealed. The shortage of US dollars is a shortage of balance sheet to intermediate between the suppliers of US dollars (mainly onshore) and the consumers of US dollars (mainly foreign investors who wants to buy US assets usually on a hedged basis). Volcker rule causes problems because it bans speculative books. In other words, banks must run matched books, i.e. borrow via FXS and lend via FXS. This makes monetary transmission expensive because an unregulated third-party intermediary must get involved to do the speculative book leg – i.e. borrow from cash pools and lend on via FXS. The Fed Vice Chairman is paying attention: “Federal Reserve Vice Chairman Randal Quarles says U.S. financial regulators are working quickly to make “material changes” to the Volcker Rule” https://www.bloomberg.com/news/articles/2018-03-05/volcker-rule-to-undergo-material-changes-fed-s-quarles-says

Given the broken monetary transmission today, it really does not really matter if the Fed hikes 25 or 50bps. It also does not really matter if the Fed’s infamous “dot plot” shows 3 or 4 rate hikes in 2018. What really matters is to fix the broken monetary transmission in a year when offshore US dollar liquidity is being drained by both US corporates and the Fed herself.

Good luck in the markets.

Post navigation