SINGAPORE WEEKLY : THE INCONCEIVABLE GDP

Remember to be a Singapore economist is to be Politically Correct & Cautiously Optimistic ?

https://tradehaven.net/market/fx/singapore-rates-weekly-being-politically-correct-and-cautiously-optimistic/

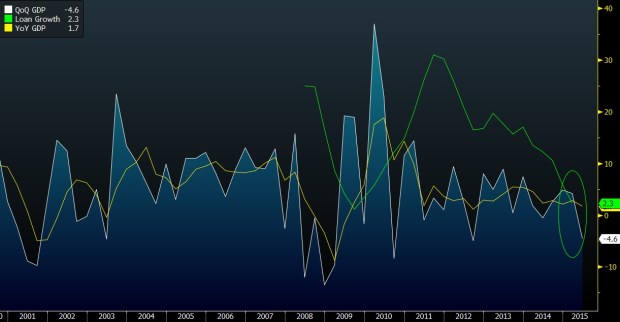

So, tell me who would dare forecast this -4.6% QoQ GDP number ?

Ranking of Economists

1. OCBC -4.3%

2. Dai-Ichi Life -3.9%

3. BofA -3.7%

4. Citibank -3.6%

5. Nomura/DBS -2%

And the next question, if 2Q15 is bad, how would 3Q15 look with the Chinois effect ?

I threw in the Loan Growth for comparison and it is worthwhile to observe that loan growth does precede quarterly dips.

Running 10 year quarterly correlations, I had a surprising find. That GDP is mostly closely and negatively correlated to the URA Singapore Property Price Index ! The QoQ GDP at -0.62 and YoY at -0.41, while having little effect on the CPI or the STI Index or the USDSGD.

To be constructive and circumspect, there is much good in this number.

1. It is election time and time for people to think hard from not just their hearts, but their pockets and piggy banks !

July 14 (Business Times) — Singapore

THE committee that reviews the boundaries for election in Singapore was formed two months ago in May and is now preparing its report, Prime Minister Lee Hsien Loong told parliament on Monday.

Revealing this in response to queries by two members of parliament, Mr Lee said that he had asked the Electoral Boundaries Review Committee (EBRC) to consider the population shifts and housing developments since the last boundary delineation exercise.

He also asked for smaller group representation constituencies (GRCs) in order to reduce their average size to below five members, and to have at least 12 single member constituencies (SMCs). Currently, there are 15 GRCs with a total of 75 MPs, as well as 12 SMCs.

2. I have been expecting some economic stimulus and now I can expect it with more confidence.

3. Pockets of opportunities in investment to emerge – e.g. if people start tightening their belts, maybe they will watch more TV ? (Starhub ?)

I believe we have seen the highs for SIBOR as far as this year is concerned as I said last month. “I think we have seen the highs for the first half of 2015 with Sibor and SOR to remain nicely contained from here and the SGD to drift within mid NEER. In addition, I believe the markets are better prepared to cope with the new ranges and hear that banks have put in some “measures” to prevent sudden run-ups even if nobody is prepared to bet on lower rates.”

https://tradehaven.net/market/singapore-rates-weekly-2-june-2015/The implication on the USDSGD is a little more tricky and thus, interest rates.

Today we have economists running for the “possible easing in October” call out of the MAS just to drum some excitement into our lifeless markets because we last heard from them in May that the policy stance will remain unchanged.

Looking at the chart below, I believe the market is quite cleaned out and what we had in the early part of the year was an exodus of excess positions which is unlikely to take an interest in the market again, for the time being and without any good reason to, not when the only possibilities are for further weakness or nothing.

How far out can you push the USDSGD to, would really depend on whether the rest of the NEER basket is going and in that case, would it not make more sense to punt on the USDJPY or the EUR instead ?

The bond market had a V shaped week, starting with a rally that cumulated in a sell off for yields to close unchanged, a better performance than the US treasury market which corrected with a vengeance.

I do not see the bond curve much at risk, at our lofty highs in yields although I feel that we shall not be seeing any enthusiastic nor aggressive buying for any reason.

Some are projecting the 10Y UST to a higher range of 2.5-3% for year end, which makes sense if we are going to see a hike in the next 6 months. That gives some space for the SGS long end yields to rise and it would be nice to have the 20Y and 30Y catch up to current US levels of 3.25% in time.

Good luck !

The Singapore June 2015 manufacturing PMI is back to expansion zone. It should be good for Q3 GDP.

🙂 Yes it is 51.1 expansionary, but still consistently below 2014’s average of 53.5, not sure how far base effect goes for PMI….