Singapore Interest Rates – The Over Worrying Nation

I had this idea to write about this for some time but held back because I wanted to enjoy the joke privately for a while longer before sharing the laugh with readers and friends.

I find it strange that Bloomberg lists Singapore as a developed market for all purposes except for its currency, the SGD dollar, which falls into the EM (emerging market) category. It stands to reasons because the SGD is not an international currency i.e. no complete freedom in cross border flows, if you remember about what I wrote a week or two back that Section 757 prevents SGD from leaving the shores.

So how dumb can it get and why is nobody, especially the media, complaining that other AAA countries like Denmark and Switzerland are now down to their most negative interest rates in history while Singapore is bucking the trend in a BIG WAY, with rates rising RELATIVELY MORE than countries like Brazil and nominally much more than countries like the US, which is the SGD NEER is mostly based upon ?

If we are in a currency war of easing, Singapore must be fighting the opposite battle.

Yet, surely the architect and engineer behind our unique monetary system, must be aware of that.

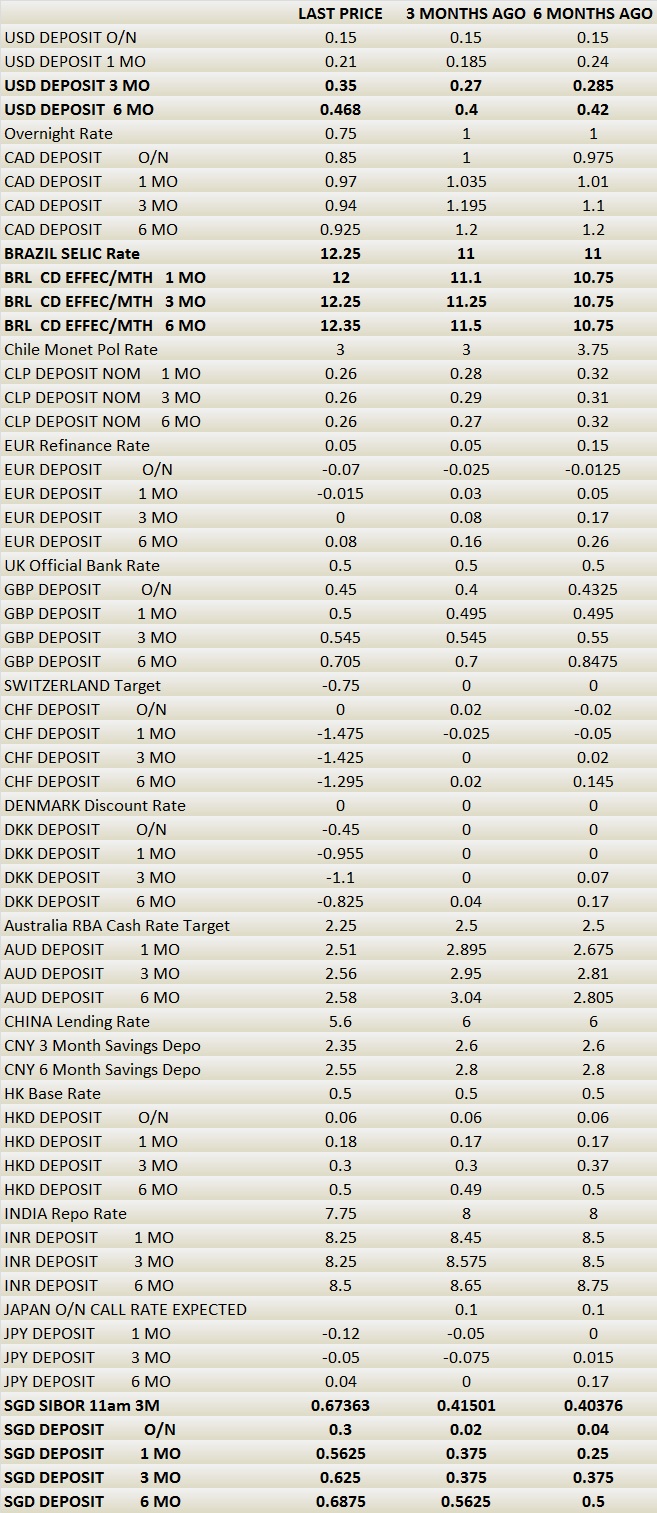

Take a look at the global snapshot where I took the liberty of highlighting the countries whose rates are higher than they were 6 months ago.

Yes. 1 month rates have more than doubled ! And overnight call rate is up 750% from 0.04 to 0.3% yesterday.

Singaporeans – A sheepish smile ? Or to glow with pride ?

We are so special aren’t we ? Or are we just the over worrying type, always worried about something (just like our founding fathers before us ) ?

Projecting the 3 month interest rates into the future.

And it looks like this on a graph.

3M Sibor and 3M Libor projected into the future

Singapore has pre-empted the FED and Janet Yellen all the way till Apr-Jul 2017 ! (note that the 3 month rate you see for Jul 2015 represents the 1 Jul – 30 Sep rate)

There is cause to worry for the industry experts and practitioners.

Because Singapore’s foreign reserves (thin white line) posted their steepest drop in history last year … errrr, that is because the reserves also hit their historical all time high in June 2014 ? So what’s wrong with coming off that top ?

From a year ago, the long term interest rates are much lower.

Not that the long term rates affect 99.9% of the Singaporeans out there because mortgage rates in Singapore, unlike America, do not go much further than 3 years, and savings and bank deposit rates here have not improved !

What makes me laugh and laugh hard is that people that I know have read my piece on Singapore’s Unique monetary system and some tell me that it is enlightening. Yet no one has stopped and thought hard enough to ask WHY ? and instead accept it as the norm. And I will stop here because I do not want to get into trouble.

Countries with pegs, or sort of pegs like ours, have their own monetary policy rates as well so that interest rates can be used to manage inflation.

For years I have been questioning that because it is a double bonus for us when times are good but a double whammy for us when times are bad i.e. low inflation (low growth) and higher interest rates. Is it because bad times are such a vague and distant memory that it has become an unfathomable impossibility ?

And Singapore is on the losing end of the currency war because it is the only country in the world that is still sticking to an appreciation stance albeit a slower one after they changed the slope last month.

The market is now looking for a re-centreing in April, I sense from some of my conversations with traders and fund managers.

A re-centreing(lower) that will re(de)-value the SGD against the members of the NEER basket that will give the currency some breathing space and for the short terms rates to go lower because the speculative expectations for a higher USDSGD will fade and SGD can continue on its path of appreciation from a lower base. (A mind numbing and brain damaging idea if we think too much about it. )

But the gist is that with USDSGD at 1.36-1.38 and no more hope of going higher, 3M Sibor can go back to 0.5% ? (assuming the rate hikes in the US go as planned and exchange rates stick around these levels) Incidentally, the 3M Sibor fixed at a new 5 year high today ! even as the 1M, 2M Sibor, 1M – 6M SOR all did not.

And I am increasingly getting sold on that idea as I write.

************

Afternote :

Appending the forward forward bond vs irs chart showing relative values for SGS peaking in Feb 2020 and Aug 2026 vs the 2024. The irs curve looks smooth enough but steep to 2020.

Related Posts :

A Last Word : The End of Higher Sibor For Now 28 Jan 2015

https://tradehaven.net/market/fx/a-last-word-the-end-of-higher-sibor/

No Central Bank Left Behind – Singapore MAS’s Surprise MPS 28 Jan 2015

https://tradehaven.net/market/fx/no-central-bank-left-behind-singapore-mass-surprise-mps/

Forex Lesson 3 : Explaining Singapore’s Managed Fx Policy 29 Jan 2015

https://tradehaven.net/market/fx/forex-lesson-3-explaining-singapores-managed-fx-policy-system/

So, from the last chart regarding SGS, it seems safe to assume a mortgage rate of (3% + 1% spread) = 4% for quite a long time.

So as long as we do out calculation for properties based on 3.5% to 4% , and if we can afford it, we should just buy for investment!

10 year averages.

1. 1M Sibor 1.13%

2. 3M Sibor 1.24%

3. 3M SOR 1.22%

4. 6M SOR 0.97%

Buying property for investment also involves estimation of the property’s yield and I had an interesting take a few years back …

“My question is this : How much will property price come off by for a 1% up move in interest rates ? This is entirely plausible because our mortgage rates are still about 1% and moving on to a 2% handle is not an impossible scenario. It will really start to burn when it hits 3% bringing about the dreaded margin calls on those loans that are leveraged to the hilt (= sub prime foreclosure scenario).

Using rough math, 1% for 25 years = 25% more you will be paying (the amount should be less due to amortisation effect), on 80% leverage, so we have about 20% ! Unless you have a wage hike of 20% or a rental hike of 20%, the property prices should come off by 20% to equalise ?” http://52.77.202.71/market/singapore-real-estate-menopause/