Food for Thought : Let’s All Save In AUD And Pass The World’s Low Rate Problem To Them

“The welfare of each is bound up in the welfare of all.” ~ Helen Keller

This cannot be more true in the new world order.

There are 24 nations in the developed markets, 11 are in the Euro bloc. This is how it looks over a 1 year period.

The interest rates for the majority are laughable, next to nothing except for ….. Australia, Canada, New Zealand and Norway. With the exception of New Zealand which hiked 1% in a year, Israel and Sweden who both cut their rates, the rest have not done anything in the past year.

So when friends ask me what to buy, guess what I say ?

AUD.

Pretty brainless AAA bet even for Singaporeans – instant carry with massively higher yields. There is little reason for the SGD to out perform the AUD now that the RBA has little onshore reason to cut further after reading into RBA Governor Steven’s remarks last week. http://www.bloomberg.com/news/2014-08-20/stevens-says-animal-spirits-needed-to-spur-australian-growth.html

But they really should be looking outside if anyone is wondering why the AUD strength would be an impediment to growth, they should realise that German bunds yield negative up to 3 years as I type. And Australia’s frustration on their strong currency (despite mining slowdown) grows. http://www.bloomberg.com/news/2014-08-27/aussie-defiance-of-iron-ore-erodes-on-fed-bets-chart-of-the-day.html

People prefer the AUD over the flighty NZD which is really too small to accommodate the flows of the world and wonderful for a squeeze trade which is exactly what happened in the past 12 months.

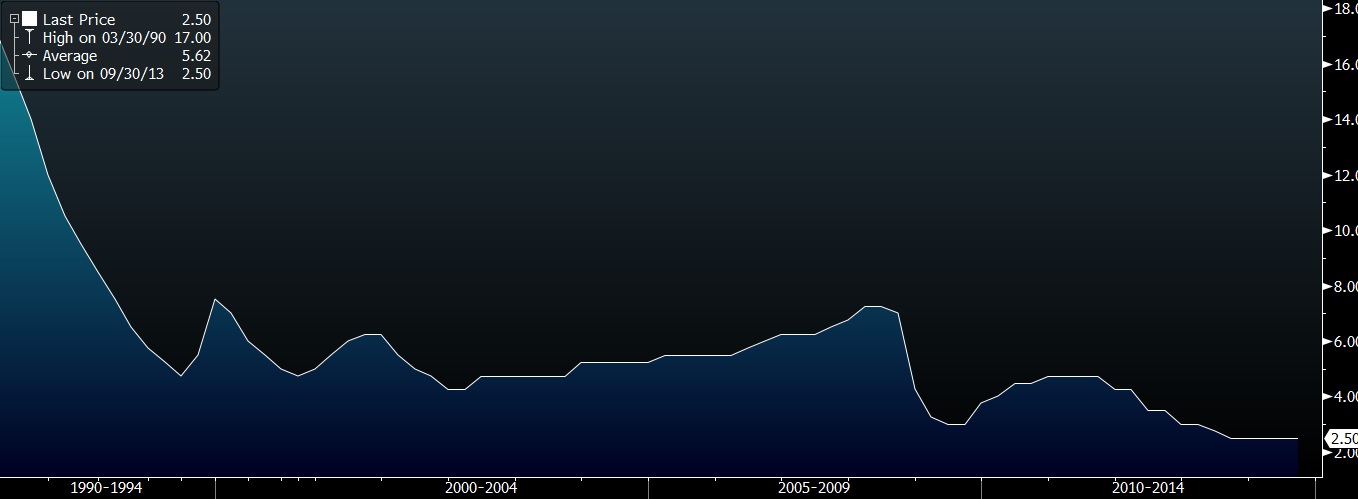

AUD bond prices are soaring, fixed income markets roaring and real estate booming (led by Singaporean investors including GIC), and the icing on the cake is that their cash rate is at a historic low of 2.5%.

With the EUR, JPY, GBP, CAD and AUD being the major currency pairs against the USD in the forex trading world, there is little to choose from if we assume a status quo in monetary policies. The ones with the most returns win, because it is just too painful to be short and losing 3% vs nothing daily.

The rest of the currencies are not such easy reads even if the returns look fantastic. The GBP and CAD for instance, have other factors at play and not as commodity based.

The SGD currency has outperformed on the year but yields are miserly. And that is what I told my friend whose wife is a new recruit to the bond investor world, deciding to follow her fellow Singaporeans’ into the sophistication of bond investment.

Just save in AUD. It will not fail you and it will be liquid enough when you see the signs to run (easy for him because he was a former FX salesperson and is still attuned to the markets). And a sure sign would be when grandparents start talking about it.

The only risk I see with the AUD is its herd mentality. My personal experience back in 2008 was a 35% loss over a 3 month long crash that dumbfounded me (AUDUSD 0.98 to 0.61). Freaking out, I did my homework and put the AUD diligently to work in the Australian stock market which netted me an equivalent 35% before quickly taking the money back in USD that caused me an opportunity loss of the AUD rebound back to 0.91 just a few months later.

The AUDUSD crash last year is particularly haunting of that 2008 episode.

I suspect the markets not over stretched yet even if open Long positions in the CFTC are at a 1 year high (much higher than GBP). The “lemming” nature of the AUD market is such that extremes are tested each time.

*note the record shorts in AUD earlier this year and last year. AUDUSD did not collapse like it did in 2008.

*note the record shorts in AUD earlier this year and last year. AUDUSD did not collapse like it did in 2008.

Thus, I daresay we can safely continue to save in AUD into our retirements, buy AUD insurance and annuities (hopefully) and pass the world’s low yield problem to them.

Developed nations are one big basket and those who persist in maintaining delectably higher rates than the nations embarking on QE are plainly asking for a currency attack…. Especially if their central banks are as helpless as the RBA.

The Germans have probably started their exodus already as their yields turn negative. EURAUD approaching its 1 year low.

Chart : EURAUD 1 year

Chart : EURAUD 1 year

AUDSGD 5 year average 1.2491, 2 year average 1.2028 and 1 year average 1.1581

Chart : AUDSGD 1 year

Chart : AUDSGD 1 year

We are sitting at 1.1660 now and its been going no where for the past 3 months. If it keeps this way, then its is a minimum 2% profit.

Should European QE erupts in a big way, the case for AUD remains intact for at least another 6 months into the potential of the first Fed hike. And the big picture remains rosy for Australia and her rich mineral earths, rich farmlands, untapped financial and services market and still-relatively-cheap real estate investments.

Good luck !

Hi Mr Tan, I am fresh graduate who just joiend an internationaI private bank. I came across your blog while I was searching DCC’s explanation on Yahoo. Your explanation on DCC gave me alot of insights into this product and has helped me undersand this product in a deeper sense. While I have read alot of DCC explanation and definitions from the web, I have to say yours is much original and written in an easy-to-understand language. Indeed, I still have some puzzles in my head regarding this product. I am hoping if you can help me? 1) From my understanding, DCC is composing of a time deposit and selling an OTM call option on deposit currency/ shorting an OTM put on the linked currency? I was told it’s always shorting OTM options but not ITM, why so? 2) Can you distinguish the differences between the risk/return profile, benefits and disadvantages when buying FX spot, FX swap, simple FX options and DCC? For example, If I am investor holding USD, and I view AUD will depreciate in 2-3 months time, I am a risk taker and want to speculate theFX market. Which FX investment tools should I go for? Buying Spot? Signing Swap, Simple FX options or DCC? I am still abit confused around the concept of different FX investment tools. Your help is much appreciated. Continue with your good blog, I would love to read updates from your blog from time to time. Best,